Tria is a self-custodial crypto spending app with a linked Visa and Mastercard that converts holdings from your wallet at the point of sale across more than 130 million merchants, with cashback up to 8 percent and built-in cross-chain trading and yield tools.

About Tria

What is Tria?

Tria is a self-custodial neobank app with a linked Visa and Mastercard payment card. You connect your crypto wallet once, and from that point you can spend directly at over 130 million merchants without selling your holdings first, bridging chains, or moving funds into a separate custodial balance. The app supports more than a thousand tokens across EVM chains, Solana, and others, including ETH, SOL, and various meme coins.

Beyond the card itself, Tria rolls trading and yield into the same app. You can swap cross-chain, trade spot or perpetuals, and earn yield on stablecoins, all from a single interface and a single self-custodial wallet. The card and the trading activity both feed into a rewards system tied to ecosystem points and the native TRIA token. The project has raised 12 million dollars, with backing from Polygon, Aptos, and Wintermute.

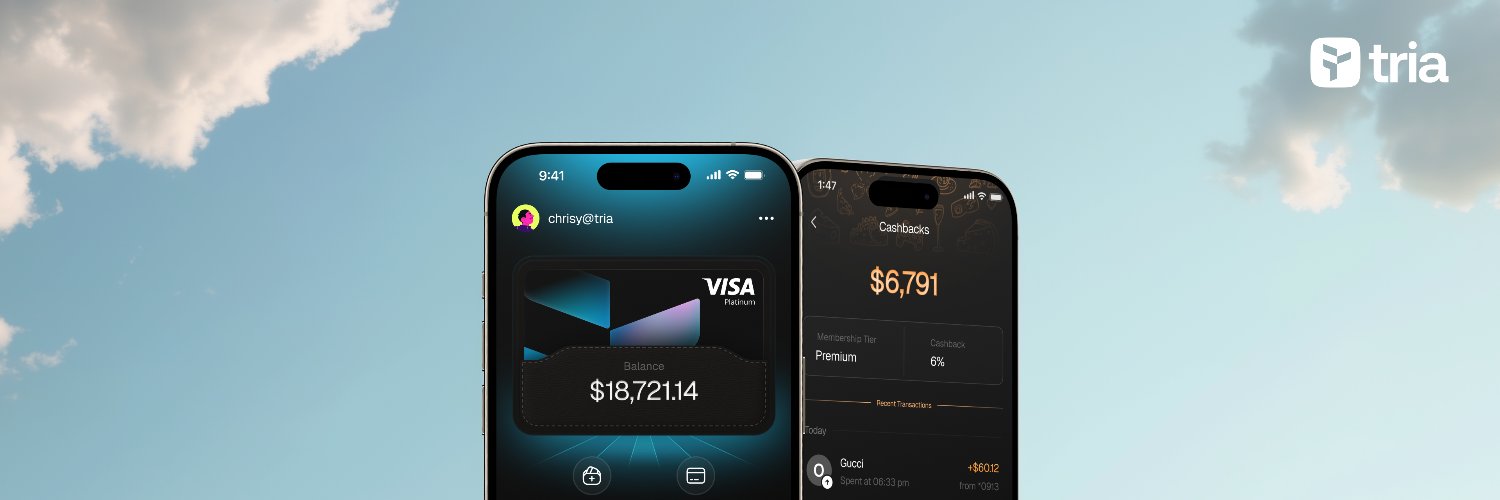

There are three card tiers. The virtual card costs around 20 to 25 dollars and gives 1.5 percent cashback, with Apple Pay and Google Pay support from the start. The Signature tier runs 90 to 109 dollars, raises cashback to 4.5 percent, and adds lounge access and ATM use. The premium metal card costs 225 to 250 dollars, offers 6 percent cashback (up to 8 percent if you stake TRIA), zero Tria FX fees on many transactions, and full worldwide lounge access. All tiers require KYC before the physical card ships.

Who uses it?

The obvious fit is someone who already holds crypto across multiple chains and wants to spend it in daily life without going through the usual steps of selling, waiting for withdrawals, and converting to fiat. If your money lives on-chain and you are tired of keeping a separate fiat account just for groceries or rent, Tria removes that step. You tap the card, the app converts just enough crypto at point-of-sale rates, and your wallet covers it in real time.

Frequent travelers get a clearer case for the higher tiers. The card works in over 150 countries wherever Visa or Mastercard is accepted, with no geographic blocks that affect some competing cards. At 4.5 or 6 percent cashback, the card cost pays itself off faster if you run regular expenses through it. Users who have tested it across Europe and Asia report smooth transactions without the friction that limits other crypto card products.

Active traders who want everything in one place are another natural fit. If you are already swapping and running perps on a daily basis, having your spending card in the same app means your rewards stack across both activities. On the other hand, if you are new to crypto, hold small amounts, or prefer a simple custodial setup with easy fiat on-ramps, the upfront card fee and KYC process may not be worth it at this stage.

How it works

When you pay with the Tria card, the app converts only what it needs from your self-custodial wallet at the moment of the transaction. Your crypto stays in your wallet until that exact instant. There is no pre-funding a separate custodial account, no manual swap before you leave the house. The conversion happens in the background using real-time rates, and the merchant receives payment like any normal Visa or Mastercard transaction.

Cashback lands in your account after each purchase. Depending on your tier, that can be 1.5 to 6 percent, or up to 8 percent with TRIA staking. The project shifted payouts to USDC rather than the native token, which most users welcomed for the stability, though it caught some off guard who had expected token holdings. Spending activity also generates ecosystem points that have fed into token allocations for early users.

The fee picture is mostly favorable but not perfectly zero. Many transactions carry no Tria FX fee, and ATM withdrawals stay free up to per-tier limits, but real-world testing shows roughly 0.5 percent on some purchases plus any underlying network costs. That is still competitive against most crypto card alternatives, and cheaper than traditional cards on foreign spend in a number of reported comparisons. A few users have flagged slower verification timelines and occasional delays on rewards for smaller accounts, so it is worth going in with realistic expectations on support response times, especially outside peak hours.

Key Features

Pros & Cons

-

Spend without pre-fundingThe card converts just enough crypto at the point of sale in real time, so your funds stay in your self-custodial wallet until the exact moment you pay.

-

Works across multiple chainsYou can spend ETH, SOL, and over a thousand other tokens including meme coins across EVM and Solana chains without manually bridging or swapping first.

-

Cashback on every purchaseDepending on the tier you choose, cashback ranges from 1.5 percent on the virtual card up to 8 percent on the metal card if you stake TRIA.

-

Accepted at 130 million merchantsBecause it runs on Visa and Mastercard rails, it works anywhere those networks are accepted, including Apple Pay and Google Pay on the entry tier.

-

Trading and yield in the same appBeyond spending, the app lets you trade spot and perpetuals or earn yield on idle stablecoins, so you are not maintaining separate accounts across multiple platforms.

-

Tiered access costs money upfrontYou pay 20 to 109 dollars just to get the card before spending a cent, and the best cashback rates are locked behind the highest tier which requires staking TRIA on top of that purchase price.

-

TRIA token dependency for top rewardsThe 8 percent cashback rate requires staking the native TRIA token, which means your reward potential is tied to the price and availability of an asset that went live only recently.

-

Self custody adds user responsibilityBecause your keys stay in your control, there is no account recovery team to call if you lose access to your wallet, and any mistake in key management means permanent loss of funds.

-

Real time conversion rate exposureEvery purchase converts crypto at the moment of sale, so in a fast-moving market you could end up spending more of your holdings than expected if prices drop between when you tap and when the transaction clears.